The Short Answer: An audited financial statement is a company’s financial report that has been examined and verified by an independent certified public accountant (CPA). This verification process provides stakeholders with reasonable assurance that the financial statements are free from material misstatements and fairly represent the company’s financial position in accordance with accounting principles.

Audited financial statements serve as the foundation of trust in business relationships. When lenders consider loans, investors evaluate opportunities, or regulators oversee compliance through the audit process, they rely on these verified financial reports to make informed decisions.

Public companies must have audited financials by law, while private companies often need them to secure financing, attract investors, or prepare for sale.

In this article, we’ll explore:

Table of Contents

Understanding the Components of Audited Financial Statements

An audited financial statement contains several standard components that work together to present a complete picture of an organization’s financial position. Let’s examine each major section and what it reveals about a company’s financial information.

Balance Sheet Components

The balance sheet provides a snapshot of what a company owns and owes at a specific point in time.

Assets listed on the balance sheet include:

-

Current assets like cash equivalents and inventory

-

Long-term assets such as buildings and equipment

Liabilities show both:

-

Short-term obligations, like accounts payable

-

Long-term commitments such as mortgages or bonds

Shareholder equity represents the company’s net worth, calculated by subtracting total liabilities from total assets. (Assets – Liabilities = Shareholder Equity)

Income Statement Breakdown

The income statement shows profitability over a specific fiscal year. Revenue recognition principles determine when sales are recorded, while expenses are matched to the periods they help generate revenue.

This includes:

-

Operating revenues

-

Cost of goods sold (COGS)

-

Operating expenses (OpEx)

-

Other income or expenses

-

Net income or loss (NI)

Cash Flow Statement Analysis

The cash flow statement tracks money moving in and out of the business through three key activities:

-

Operations - Cash flows from daily business activities

-

Investing - Equipment purchases or sales

-

Financing - Loans, stock issuance, or dividend payments

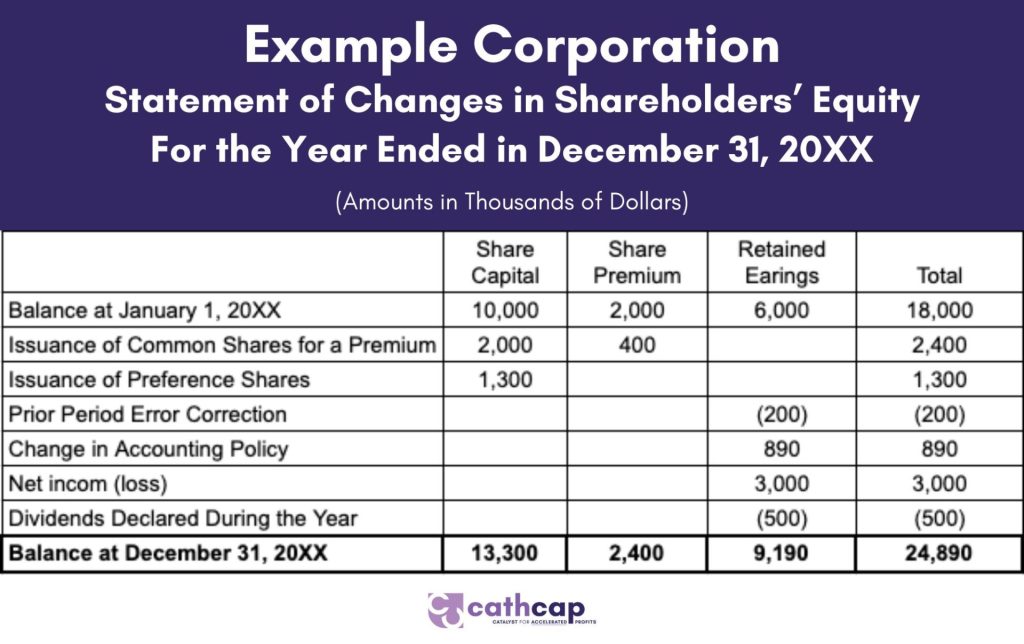

Statement of Changes in Shareholders' Equity

The statement of changes in shareholders’ equity shows how ownership value has changed over the reporting period. This statement bridges the gap between the balance sheet and income statement by explaining what caused equity to increase or decrease.

Key components include:

-

Beginning equity balance - Starting point from the previous period

-

Net income or loss - Profit or loss from the income statement

-

Dividend payments - Cash distributions to shareholders

-

Stock transactions - New shares issued or shares repurchased

-

Other comprehensive income - Items like foreign currency adjustments or unrealized gains/losses

This statement helps stakeholders understand whether equity changes came from profitable operations, new investments, or other factors affecting shareholder value.

Notes and Supplementary Information

The notes section provides additional context about accounting principles, debt terms, and significant events affecting the financial statements. These detailed explanations help readers understand unusual items or accounting standards.

Supplementary schedules might include detailed breakdowns of:

-

Inventory

-

Fixed assets

-

Investments that support the main financial report

Each component undergoes thorough examination during the audit process, with auditors verifying accuracy and compliance with accounting standards.

The Audit Process Explained

Pre-Audit Preparation

The audit process follows structured standards that start long before auditors arrive. During this phase, companies gather extensive documentation including:

-

Financial statements

-

Balance sheet records

-

Accounts receivable and payable records

-

General Ledger

-

Income statement data

-

Tax returns

Management also prepares detailed explanations of their internal control systems and accounting principles.

Internal Controls Review

When auditors begin their work, they first review the company’s internal controls in accordance with best practices. This involves examining how the organization:

-

Handles financial reporting

-

Maintains separation of duties

-

Implements security measures to protect assets and financial information

Auditors document these controls and test their effectiveness through walkthroughs and control testing procedures.

Substantive Testing

The core financial statement audit procedures involve substantive testing, where auditors examine individual transactions and revenue balances in detail. They select samples of financial records and trace them through the accounting system to verify accuracy.

Analytical procedures complement this work by comparing financial ratios and trends across previous fiscal years to identify unusual patterns or discrepancies that warrant investigation.

External Verification

Verification extends beyond reviewing financial reports. Auditors take several verification steps:

-

Send external confirmations to banks, customers, and vendors to independently verify cash flows and transaction details

-

Conduct physical observations of inventory counts and asset existence

-

Verify the physical existence and condition of property or equipment

Documentation and Reporting

Throughout the process, auditors maintain extensive documentation of their work. This includes:

-

Detailed work papers showing testing procedures

-

Sample selections and the auditor's opinion

-

All significant findings and adjusting journal entries

-

Any identified control deficiencies

This documentation serves as evidence supporting the final annual report and may be reviewed by regulators or other parties.

Types of Audit Opinions and Their Significance

An audit opinion represents the auditor’s professional judgment about a company’s financial statements. Understanding these opinions helps stakeholders make informed decisions about their involvement with an organization.

Unqualified Opinion

An unqualified opinion, also called a clean opinion, indicates that the audited financial statements present information fairly and follow accepted accounting principles. When auditors issue this opinion, they confirm that the company’s financial reports are accurate and transparent.

This opinion type gives investors and lenders confidence in the organization’s financial position.

Qualified Opinion

Auditors issue qualified opinions when they find specific issues with certain accounting practices or cannot verify particular financial statements. This might happen when:

-

A company uses accounting methods that differ from standards in some areas

-

Auditors cannot gather enough evidence about specific transactions

While concerning, a qualified opinion does not necessarily indicate major problems with the overall financial health of the organization.

Disclaimer of Opinion

Sometimes, auditors cannot form an opinion about financial statements. This leads to a disclaimer of opinion, which occurs when auditors lack access to necessary financial information or face significant limitations in their audit scope.

For example, if a company cannot provide adequate documentation or restricts access to certain records, auditors may issue this opinion. A disclaimer tells stakeholders that the reliability of the financial statements cannot be determined.

Building Financial Confidence Through Professional Auditing

Audited financial statements represent the highest level of assurance in financial reporting, providing stakeholders with independently verified financial information they can trust. These financial statements serve as a foundation for informed business decisions and relationships.

The benefits of audited financial statements extend beyond basic compliance with accounting principles, they boost your company’s credibility with investors, lenders, and business partners. These financial reports help secure better financing terms, attract potential investors, and demonstrate your commitment to transparency.

Ready to Strengthen Your Financial Reporting?

Professional audit services can guide you through the process and help you navigate the complexities of financial compliance. Start by gathering your financial records, reviewing your internal controls, and consulting with experts who can assess your specific needs.

Cathcap specializes in comprehensive financial solutions that go beyond traditional auditing. Our team offers:

-

Financial statement preparation and review services to ensure your reports meet the highest standards

-

Internal controls assessment to strengthen your financial processes

-

Compliance consulting to help you navigate regulatory requirements

-

Strategic financial planning to position your business for sustainable growth

Taking this step toward financial transparency positions your business for growth and builds lasting trust with stakeholders. Whether you’re preparing for investment, seeking financing, or simply want to enhance your financial credibility, professional guidance makes all the difference.

Contact us today to discuss your financial reporting needs and discover how our tailored solutions can strengthen your business foundation.

Recent Comments