The Short Answer: To prepare your business for a recession, build a cash reserve, protect profit margins, and secure financing options before an economic downturn hits. Use simple weekly cash flow visibility and clear decision rules so you can move fast in uncertain times.

A recession is a period of temporary economic decline during which trade and industrial activity are reduced, generally identified by a fall in GDP in two successive quarters, though in the U.S., the NBER officially designates recessions based on a broader set of indicators. It is tracked across indicators like employment, consumer spending, real income, gross domestic product, and industrial production.

Table of Contents

Build cash and see it clearly

Goal: Keep your business funded through tough times. Your plan should work across different scenarios, from a mild slowdown to a possible recession.

1) Make a 13-week cash flow forecast

A 13-week cash flow forecast gives business owners clear visibility into upcoming inflows and outflows. Tracking invoices, payroll, taxes, rent, debt payments, and planned purchases week by week helps you spot gaps before they become crises.

Tagging each line item as fixed, variable, or deferrable makes recession planning faster and more effective, since you’ll know exactly which expenses can be adjusted in tough times. This kind of detail gives you a realistic roadmap to protect cash flow during an economic downturn.

2) Set a realistic cash reserve

Many small business owners operate with minimal emergency savings, leaving them vulnerable when economic activity slows. A practical cash reserve, sized to your business model and seasonal patterns, acts as a buffer against revenue drops or delays that can follow higher unemployment and reduced consumer spending.

Rather than trying to fund it all at once, phase your savings in over time so it doesn’t strain current operations. The goal is to build an emergency fund that allows you to weather uncertain times and keep your balance sheet steady.

3) Collect Owed Cash Quickly & Delay Payments Out (Where Possible)

Speeding up receivables while slowing payables can significantly strengthen cash flow during a potential recession. Invoicing immediately upon delivery, offering ACH or card links, and providing small early-pay discounts encourage faster payments. Review and align AP terms to industry norms (often 30–45 days) to smooth outflows and batching vendor payments reduce unnecessary leaks and fees, giving you more control over working capital.

Managing excess inventory through ABC analysis and tighter reorder points also frees up cash that would otherwise be tied up on shelves, helping small businesses avoid difficult times.

4) Add flexibility before the next recession

Flexibility is one of the strongest defenses against a financial crisis. Expanding a revolving line of credit while business results are strong creates a cash buffer you can tap if conditions shift. Terming out near-maturity debt prevents a lump-sum squeeze on your balance sheet, while keeping financial statements organized reassures banks and potential investors.

If demand drops, some states offer Short-Time Compensation (STC) programs that allow you to reduce hours instead of jobs, preserving customer relationships and employee loyalty while still cutting costs during a possible recession.

Cash Levers

|

Lever

|

What to do

|

Why it helps

|

|---|---|---|

|

Accounts receivable (AR)

|

Early-pay offers, automated reminders

|

Pulls cash forward and stabilizes cash flow

|

|

Accounts payable (AP)

|

Normalize payment terms, batch runs

|

Smooths outflows and protects the bottom line

|

|

Inventory

|

ABC analysis, adjust reorder points

|

Reduces excess inventory and frees working capital

|

|

Capex

|

Stage non-core capital projects, use ROI thresholds

|

Preserves cash for the core revenue stream

|

|

Debt

|

Expand revolver, refinance maturities

|

Adds room to maneuver in difficult times

|

Protect Sales & Margins While Keeping Growth Alive

Goal: Hold the line on unit economics without damaging customer relationships or long-term growth opportunities.

Customers and pricing

Protecting sales during an economic downturn starts with understanding which customers drive your bottom line. Segmenting accounts by profitability and risk allows you to prioritize service levels for core clients, building stronger customer loyalty when times get tough.

At the same time, tightening discount approvals and using value-based packages helps safeguard profit margins without alienating buyers. Offering smaller bundles or shorter-term contracts can also keep potential clients engaged when consumer spending slows, creating flexibility without losing revenue streams.

Smart cost moves

Managing business expenses wisely is critical in uncertain times. Sorting costs into protect, flex, and pause categories helps you identify what drives revenue and what can be delayed or eliminated.

Standardizing workflows and automating repeat tasks reduces inefficiencies, lowering costs while keeping operations consistent. In addition, consolidating vendors where it improves unit pricing and quality can free up cash flow while still supporting growth opportunities, making your business model more recession-proof.

Keep your team intact

A small business owner knows the value of retaining skilled employees, even during a significant decline in demand. Instead of cutting staff outright, consider work-sharing programs where reduced hours are supplemented by unemployment benefits, allowing you to keep talent while reducing payroll strain.

Cross-training employees and documenting procedures ensure business continuity if workloads shift, while voluntary PTO programs create flexibility without sacrificing long-term customer relationships or team morale. Preserving talent through difficult times positions you to accelerate faster when the next recession eases.

Supply, stock, and delivery

Supply chain resilience can make the difference between meeting demand and losing business in a possible recession. Applying ABC inventory analysis helps you trim slow-moving products and right-size safety stock, ensuring cash isn’t tied up in excess inventory.

Dual-sourcing critical items and reviewing lead times quarterly protects you against disruptions that could hurt customer relationships. Finally, aligning replenishment to actual demand with smaller, more frequent orders gives you agility to adapt to changing economic conditions while still protecting your profit margins.

Lock In Capital & Options

Goal: Stay bankable, deal-ready, and steady if the U.S. faces an economic recession. Banks and buyers prefer clean data and clear plans.

Be financing-ready

-

Meet your banker now with a concise package: 13-week cash forecast, year-to-date (YTD) results, trailing 12-month (TTM) financial statements, and a simple uses-of-funds plan.

-

Map covenants and your headroom. Set early-warning triggers.

-

Keep Uniform Commercial Code (UCC) filings, asset lists, and agings clean. This reduces approval friction when you need financing options.

Strengthen the balance sheet

-

Shorten the cash conversion cycle with faster AR, normalized AP, and better inventory turns.

-

If you carry variable-rate debt, consider refinancing into fixed terms to reduce exposure to Federal Reserve policy shifts on interest rates.

-

Review risk transfer tools like key-person, business interruption, cyber, and trade credit insurance.

The 2024 Small Business Credit Survey shows more firms reported revenue decreases than increases over the prior year, which is another reason to prepare early and keep optionality high.

Build a 90-Day Operating Cadence You Can Run in Any Downturn

Turn recession planning into simple habits that protect cash flow, margins, and your bottom line. This cadence helps a business owner or small business stay steady in uncertain times without slowing growth.

Weekly (30–45 minutes)

-

Cash huddle: Review the 13-week forecast, receivables aging, and payables by due date. Decide who will collect, what to defer, and how much to add to the cash reserve.

-

Pipeline check: Look at qualified demand, win rates, and near-term starts. If coverage drops, shift marketing efforts to proven channels and activate retention plays to protect the revenue stream.

-

Working capital moves: Tighten payment terms where appropriate, batch vendor runs, and clear excess inventory that ties up cash.

-

Customer health: Scan at-risk accounts, usage or delivery issues, and renewals. Assign one owner for each follow-up to strengthen customer relationships and loyalty.

Monthly (60–90 minutes)

-

Margin and pricing review: Compare actuals to target by product, service, or client. If profit margins slip, simplify offers, set clear minimums, and pair pricing with visible value.

-

Expense review: Sort spend into protect, flex, and pause. Keep what supports sales and delivery, pause non-essentials, and renegotiate contracts where you can.

-

Balance sheet tune-up: Check inventory turns, debt maturities, and covenant headroom. Clean books and organized financial statements help with financing options and potential investors.

-

Policy refresh: Revisit credit policies, return rules, and project scopes. Small clarifications reduce leaks fast.

Quarterly (2–3 hours)

-

Scenario testing: Run 3–4 different scenarios that reflect the economic situations you could face: flat demand, a 10% dip, a faster rebound, or a possible recession.

-

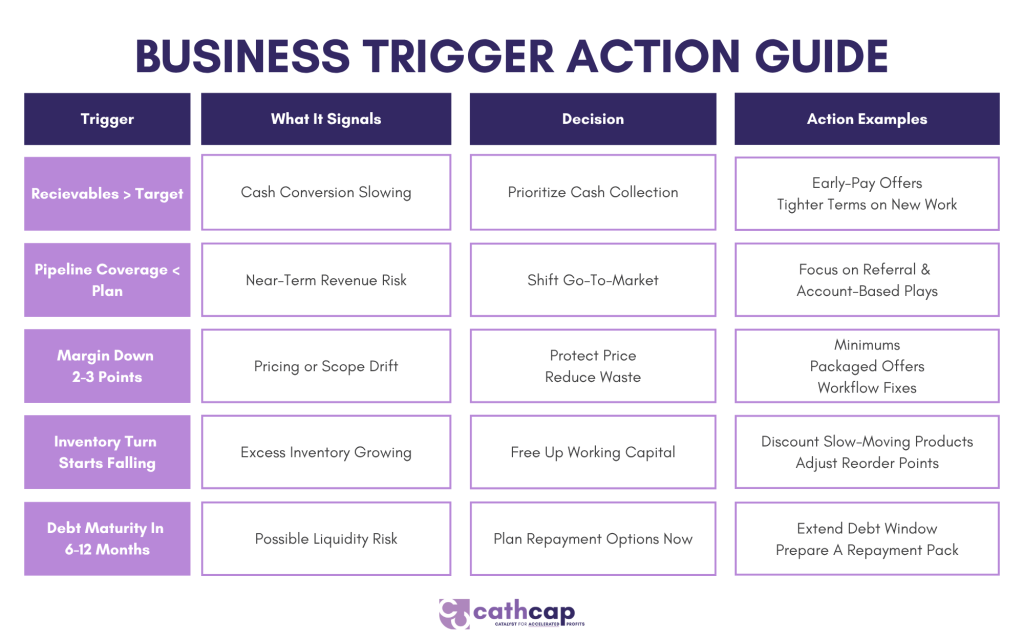

Trigger map: Define simple tripwires that tell you when to act, not just monitor. Examples: days-sales-outstanding rises above target, pipeline coverage drops below plan, or inventory turns fall.

-

Capital check-in: Review bank relationships and credit capacity. Monitor central bank policy and interest rates, including Federal Reserve moves in the United States, and plan responses for rate changes.

-

Opportunity scan: List growth opportunities that appear in an economic downturn: partnerships, selective hires, or small acquisitions. Decide the thresholds that would make a move attractive.

Simple Trigger/Action Guide

Immediate 30-60-90 day action roadmap

-

Days 1–30: Stand up the weekly cash huddle, clean aging reports, standardize payment terms, and publish a one-page scorecard tracking cash, pipeline, and customer health.

-

Days 31–60: Run scenario tests, set trigger thresholds, and align leaders on who decides what when conditions change.

-

Days 61–90: Negotiate vendor and banking terms, right-size stock levels, tighten handoffs in delivery, and refresh your customer retention plan.

Why this cadence works

-

It keeps decisions close to cash, which matters most in a recession or potential recession.

-

It balances defense and offense, so you protect today while staying ready for new products or growth opportunities.

-

It is portable across business models. Product, services, and real estate operators can all use the same rhythm with minor tweaks.

-

It builds lender and buyer confidence. Clear routines, clean data, and quick responses signal strength when financing options are tight.

You should run this check-in even when times are good. You will spot problems earlier, can adjust faster during an economic downturn, and be better positioned when the next issue arrives.

Stay Resilient During Recessions

Recessions test cash, margins, and access to capital. The businesses that prepare early, measure what matters, and act on leading signals navigate difficult times with less stress and better outcomes. In short, recession planning is about cash flow visibility, a right-sized cash reserve, and flexible financing options.

Next steps with Cathcap: We deliver hands-on finance leadership that strengthens cash flow, protects margins, and keeps you bankable in uncertain times. Our services span strategic planning and scenario thinking; working capital and pricing strategy; banking and capital advisory; and operational performance improvement across teams. For owners navigating change, we help guide stakeholder alignment while maintaining day-to-day execution.

Recent Comments